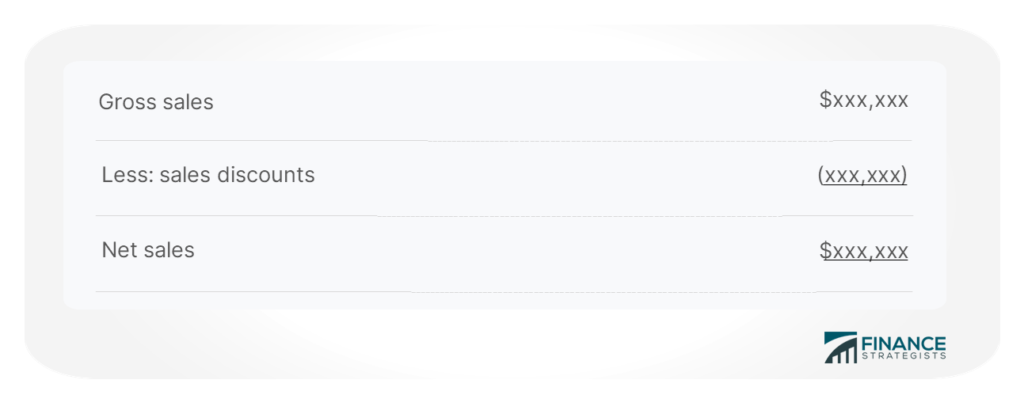

This means that the business would collect and remit less tax on sales where discounts have been applied. It is essential for businesses to adjust their tax calculations to reflect these discounts to avoid underpaying or overpaying taxes. Most businesses do not offer early payment discounts, so there is no need to create an allowance for sales discounts. By doing so, you can immediately reduce sales by the amount of estimated discounts taken, thereby complying with the matching principle. A company may choose to simply present its net sales in its income statement, rather than breaking out the gross sales and sales discounts separately. This is most common when the sales discount amount is so small that separate presentation does not yield any material additional information for readers.

- For instance, if a customer buys 100 units at $10 each with a 5% discount, the journal entry would debit Accounts Receivable and credit Sales Revenue for $950.

- However, a company may decide to just simply record its net sales in its income statement, rather than reporting the sales discount and gross sales separately.

- Trade discount refers to the reduction in the price of a commodity or service sold to wholesalers at the time of bulk purchases.

- For example, if a product listed at $1,000 is sold to a retailer at a 10% trade discount, the journal entry would debit Accounts Receivable and credit Sales Revenue for $900.

GAAP Expense Recognition Principles for Financial Accuracy

Using the same example, the initial entry would debit Accounts Receivable and credit Sales Revenue for $980. This method provides a more conservative approach, reflecting the anticipated cash inflow more accurately. The business receives cash of 1,950 and records a sales discount of 50 to clear the customers accounts receivable account of 2,000. The tax implications of sales discounts are an important consideration for businesses.

Sales Discount Journal Entry

A Cash or Sales discount is the reduction in the price of a product or service offered to a customer by the seller to pay the due amount within a specified time period. When you’re dealing with a multitude of payment processing platforms—Stripe, PayPal—and ecommerce platforms like Shopify, manually tracking every discount can quickly become a nightmare. Not only does it eat up your time, which is already worth its weight in gold, but it also opens the door to mistakes, all of which can distort your financial statements. Suppose you’re selling $1,000 worth of products to a regular customer, and you offer a 10% trade discount. It’s already been briefly mentioned that a trade discount is a price reduction given to customers at the time of the sale. It’s usually based on the volume of goods purchased or the customer’s business relationship.

Journal Entries

Trade discounts, unlike cash discounts, are not recorded separately in the accounting books. The sale is recorded at the net price after the discount, simplifying the accounting process. For example, if a product listed at $1,000 is sold to a retailer at a 10% trade discount, the journal entry would debit Accounts Receivable and credit Sales Revenue for $900. This approach ensures that the financial statements reflect the actual revenue earned from the sale, without the need for additional entries to account for the discount. Adjusting the accounts receivable to reflect sales discounts is a nuanced process. It involves updating the ledger to represent the reduced amount that a business expects to collect from its customers.

How to Sell on Amazon Without Inventory: 4 Main Methods Explained

This means that the buyer can satisfy the $900 obligation if it pays $891 ($900 minus $9 of sales discount) within 10 days. The best practice to record a sales entry is debiting the accounts receivable with full invoice and credit the revenue account is sales discount an expense with the same amount. Sales discounts are a common strategy businesses use to incentivize prompt payments or move inventory quickly. While they can be effective for these purposes, they also introduce complexity into financial reporting.

How Synder can automate your sales discounts

If the GP has absolute power then the discount for lack of control is zero. However, the GP still gets the discount for lack of marketability, which could be between 10%-20%. Cash and marketable securities with a likely short holding period would have the lowest discount for lack of marketability. The longer the expected holding period of the assets, the higher the discount for lack of marketability and vice versa. An expense is an operational cost that a business incurs in order to generate revenue.

For example, terms of “1/10, n/30” indicates that the buyer can deduct 1% of the amount owed if the customer pays the amount owed within 10 days. As a contra revenue account, sales discount will have a debit balance and is subtracted from sales (along with sales returns and allowances) to arrive at net sales. When a sales discount is offered to few customers, or if few customers take the discount, then the amount of the discount actually taken is likely to be immaterial. In this case, the seller can simply record the sales discounts as they occur, with a credit to the accounts receivable account for the amount of the discount taken and a debit to the sales discount account.

If the entity has a distribution history the discount would be at the lower end. If the entity has no distribution history, the discount would be at the higher end. A 90% LP interest has a lower discount for lack of control than the 1% LP Interest. This means depending on the distribution of the stock, a block could have the potential to gain a premium price over a pure minority value because of its potential as a swing block.

However, these cash reductions offered to customers have an effect on a company’s financial statements so they must be recorded as a reduction in revenue under the line item called accounts receivable. As seen in the income statement above, the sales discount is a contra-revenue account and not an expense. As a contra revenue account, the sales discount appears on the income statement as a $5,000 reduction from the gross revenue of $100,000 that ABC Ltd reported, which results in net revenue of $95,000.

In this blog, I discuss the main factors that have a material impact on the above discounts. I also bring a few examples and discuss briefly the magnitude of the discounts we regularly apply. To determine the discounts, it is necessary to review carefully the legal documents of the entity such as the Partnership Agreement, Operating Agreement, or Bylaws.

The first is to create a “contra-revenue” account and the second is to simply net the discount immediately off of the Revenue figure. A contra-revenue account is not an account that is shown in the entity’s Financial Statements. It is simply a placeholder account that the entity uses to keep track of their discounts. When preparing the year-end financial statements, the contra-revenue account is netted from the Revenue account, resulting in a Revenue figure net of all discounts. To illustrate a sales discount let’s assume that a manufacturer sells $900 of products and its credit terms are 1/10, n/30.